Two Roads to Legitimacy

There are now two different types of regulators that oversee sports trading. Who is better equipped to regulate the growing vertical?

The U.S. sports trading landscape has become a fascinating dichotomy. Several distinct regulatory pathways have emerged to allow venues to offer Americans a chance to trade on sports event contracts; the federally regulated Designated Contract Market (DCM) overseen by the Commodity Futures Trading Commission (CFTC), and the state-by-state licensed Online Sportsbook (OSB).

While both models share significant common ground, their operational realities, economic structures, and ultimate consumer experiences diverge significantly.

Recent statements by the likely incoming Chairman of the CFTC, Brian Quintenz, present a tectonic shift in the regulatory landscape. While the CFTC will look to exert oversight, several states have made it clear that they believe sports contracts constitute sports wagering, and should continue to fall under their oversight. Read about Everything CFTC Pick Quintenz Said About Prediction Markets In Senate Hearing from Dustin Gouker here.

While there exists excellent analysis relating to the legality and applicability of exclusive jurisdiction of the Commodity Exchange Act (CEA), federal preemption, and other legal matters (not the least of which would be Andrew Kim’s latest piece on Event Horizon), this article takes a different approach. In this article, we’ll evaluate nearly every aspect of creating a regulatory structure for sports event contracts, from licensing and market access, match integrity, consumer protection, and the ability for operators to innovate and continue to grow the market.

The inspiration for this article comes from a quote from the Pennsylvania Gaming Control Board (PGCB) in their official public comment to the CFTC:

“With all due respect to this body, it would take years for the CFTC to create the regulatory system and oversight that state gaming authorities have in place and, were you to do that, it would create a redundancy to something that already exists and works exceptionally well.”

There you have it: States feel they are better equipped to oversee sports event contracts, and if the CFTC tried to achieve parity, such an effort would take years.

But to what degree is this true?

Before we proceed, it’s important to make clear that a sportsbook is not a sports prediction market. A prediction market is a market, while a sportsbook is, well, not a market at all.

In this article, we’ll explore which regulatory body, the CFTC versus States, is better equipped to regulate this new vertical.

Regulatory Approach

CFTC

The CFTC employs a “risk-based” regulatory approach, prioritizing areas with the highest potential for harm. This enables the agency to direct its resources according to risk and impact. Although this method offers greater flexibility and adaptability, it demands a higher level of regulatory expertise and can introduce subjectivity, which may result in inconsistent or uneven oversight. At the same time, there remains a highly rigorous testing process required for market launch.

A DCM operates under a single federal license, granting access to customers across all 50 states. Governed by the Commodity Exchange Act, specifically its 23 Core Principles, the application process is exhaustive but singular. Once approved, DCMs maintain their standing through quarterly attestations of financial and compliance resources. The CFTC's staff are veterans in derivatives, sophisticated surveillance technology, and the intricacies of market microstructure, and order books.

State-Licensed OSB

State regulators typically adopt a “rules-based” framework for overseeing online sports betting. This model emphasizes strict, predefined rules that operators are required to follow. While such an approach ensures consistency, predictability, and straightforward enforcement, it lacks flexibility and has proven ill-suited for adapting to prediction markets or other non-traditional forms of sports wagering, especially those that don’t neatly fit within the conventional online sportsbook model.

An OSB must navigate the regulatory maze of each individual state where it wishes to operate. This means duplicative applications, fingerprints, background searches and detailed financial information repeatedly. This approach significantly deters new entrants, especially VC-backed start-ups that do not have massive compliance departments. Operators must regularly submit detailed data as often as daily in several jurisdictions, including wagers, promotional terms and conditions and activities, and responsible gaming measures, to each state's regulator. Historically, these state bodies have focused on brick-and-mortar casinos and are often still building expertise in the dynamics of exchange-style trading. Entry fees can be astronomical, with New York demanding a $25 million just for the license fee, for example.

The nod here goes to the CFTC for a "one-and-done" licensing process, creating a streamlined path to a national market. While there can be certain advantages for the States to have the ability to tailor rules to specific local policy goals and concerns, marketplaces work best under a single set of rules for all participants.

While innovation often outpaces rules-based regulation, the underlying intent behind innovation can be appropriately understood and deliberated by regulators taking a risk-based approach.

It’s hard to overstate just how poorly equipped the rigid, rules-based approach is in trying to stay ahead of new and innovative options in or adjacent to regulated OSB, and sports event contacts are the latest example.

Alex wrote about the importance why legislators must equip state regulators with significantly more risk-based autonomy in depth here.

Licensing & Ongoing Compliance

The financial and administrative costs of getting (and staying) licensed differ dramatically.

Up-front Costs:

CFTC: To acquire a DCM designation (license), operators pay roughly $600,000, and $100,000 per year. Operators must also undergo an extremely detailed licensing and application process, similar to launching operations in a single state. Major investors and key principals must disclose information to the Agency.

States: Licensing Costs range from around $500,000 in states like Maryland to the eye-watering $25 million in New York. This must be paid to each state separately.

Market Access:

On top of license fees paid directly to the state, operators in most states must pay other private businesses or entities- most commonly casinos- for “market access”. While it’s difficult to know exactly what this would cost for all states (likely in the $20m range), there is a significant burden upon operators to find and manage each relationship with their land-based partner. Those market access deals carry, in the aggregate, likely another $20m per year in “guaranteed revenue share” payments from the operator.

Capital Requirements:

CFTC: The CFTC mandates that DCMs maintain liquid financial resources equivalent to at least 12 months of operating costs. This is a clear, quantified, and prudent requirement. It’s important to keep in mind that DCMs do not hold capital of the trading participants. Designated Clearing Organizations (“DCO”) hold that responsibility.

States: Most states require bonds or minimum bank balances against the requirement that OSB’s must maintain to satisfy customer balances, plus the total net amount that patron open bets could win. The latter part doesn’t make a lot of sense when a prediction market doesn’t hold the risk on a transaction.

Technology & Code Certification:

CFTC: Involves certifying one primary codebase for the platform, initially, prior to launch. This is obviously a lot more fluid for a development team to avoid multiple code freezes and disruptions during a product rollout.

States: Operators may need to maintain up to 38 slightly different builds of their platform to comply with varying state regulations. Every user interface tweak or feature addition can require re-approval in multiple jurisdictions, which can easily balloon costs significantly annually in QA, lab testing, and certification. (An example of this is something as simple as how the state prefers to have their responsible gaming message and hotline resource.)

Real-World Impact:

The high fees and limited "skins" (licenses) in many states restricts the prediction market model entirely. For example, a company like Sporttrade, which aims to bring exchange principles to sports betting, highlighted its multi-year struggle to gain entry into Maryland, illustrating how the state-by-state system can stifle competition.

The nod here goes to the CFTC which provides a noticeably easier path to licensure and compliance. States have largely leveraged duplicative licensing and disclosure requirements dating back to initial physical casino licensing rules in an effort to keep the mob out of gaming. However, the unintended consequence of subjecting operators, vendors, and investors to such a painstaking and duplicative process has actually kept significant venture capital, innovation, and vendors out of their regulated markets.

Market Integrity, Product, and Surveillance

Ensuring fair and orderly markets is paramount, but the approaches differ.

Listing New Markets/Contracts:

CFTC: Can "self-certify" new contracts, meaning they can file them with the CFTC and launch them as soon as the next day. This allows for rapid innovation, but places a significant burden on the exchange to rigorously vet for manipulation risks. Currently, sports contracts on DCMs have been generally limited to simpler financial-style instruments, such as money-line “to win” contracts, though it is expected to evolve.

States: Each new wager type typically requires formal approval from state regulators, a process that can take weeks or even months, slowing down product innovation. Each state maintains a completely separate list of approved wagers, causing confusion to customers about expectations as they cross state lines. State-licensed sportsbooks offer the comprehensive menu that many sports fans have come to expect. Acceptance of events is largely focused around integrity and manipulation risk as well as preventing “negative” wagering types (such as injuries, yellow-cards, etc).

Real-Time Monitoring:

CFTC: Are required to operate sophisticated automated surveillance systems to detect and deter abusive trading practices like spoofing or wash trading. They must demonstrate the robustness of these systems to CFTC examiners.

States: States often rely more on operator self-policing and periodic audits, though this is evolving. Operators will work with integrity providers to share intelligence on potential match fixing. Sporttrade goes above and beyond and is the only OSB employing market surveillance tools (NASDAQ SMARTS).

Regulatory Expertise:

CFTC: The CFTC staff are specialists in market data analysis, order book dynamics, and complex financial instruments.

States: Many state regulatory bodies are still building their internal expertise in the nuances of exchange-style order book, given their historical focus on casino gaming.

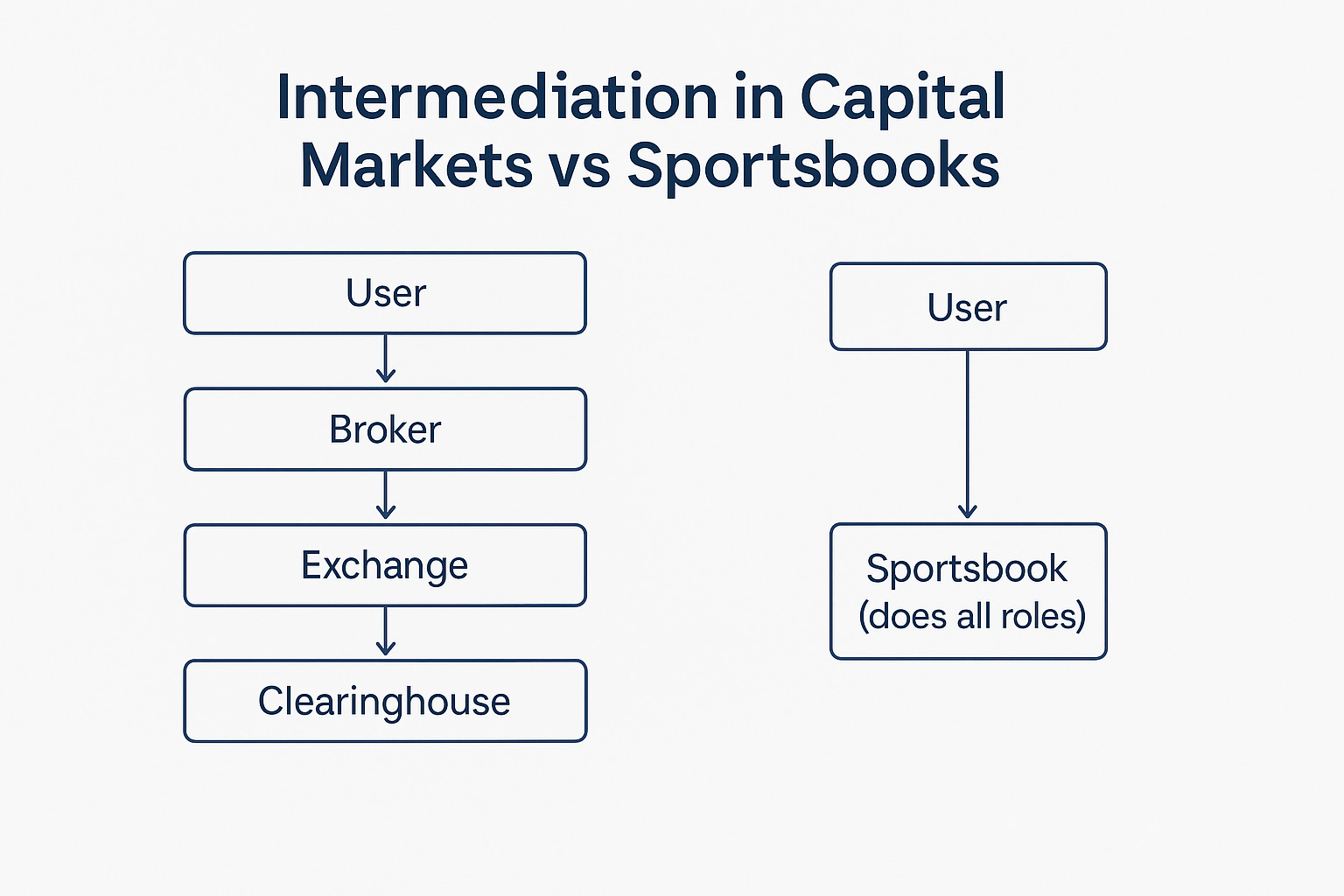

Market Structure & Intermediation

When we think about the most robust market structures in the world, we think about industries like the US equities markets.

The US equities market is an ecosystem, with each part of that ecosystem serving a unique and distinct purpose; from brokers to exchanges, clearinghouses, market makers. Some call this intermediation, a structure where a retail participant's trade touches several parts of the ecosystem, each of which effectively serve to increase participation, legitimacy, and consumer protection.

Juxtapose that with how online sportsbooks are understood and regulated, they are akin to being all things in one: the broker, the exchange, the clearinghouse, and the market maker. While this is not necessarily a bad thing when it comes to sports and event contracts, we think it would be fair to say that the sort of intermediation that is permitted and encouraged in capital and commodities markets should at least be permissible in the regulated OSB market.

States: The largest benefit to intermediation is a construct where brokers (think Robinhood, Schwab, etc.) can create the relationship with customers, and route those customer orders to venues (exchanges) to be executed. Thanks to broker intermediation, participation in stock trading is significantly higher than it would be otherwise, and such participation has led to the increasing efficiency and tightening of spreads. Unfortunately, given the rules-based nature of states, such intermediation isn’t permitted, as it’s not contemplated in the rules.

The CFTC on the other hand embraces the benefits of intermediation, with a structure that shares some similarities with the US equities market ecosystem. Some operators are brokers (known as Futures Commissions Merchants “FCM’s” or Introducing Brokers “IB’s”), some operators are DCMs, and clearing occurs on DCOs (Derivatives Clearing Organizations).

The nod goes to the CFTC here. It’s hard to think about any mature regulatory market structure that doesn’t at least allow intermediation. The existing “sportsbooks do everything” approach serves as an unfortunate deterrent against sports exchanges flourishing in the state-regulated environment.

Responsible Gaming & “Consumer Protection”

Protecting consumers, especially vulnerable individuals, is a critical responsibility. On the most recent Business of Betting podcast, Jason Trost debates with lawyer Daniel Wallach on the merits of CFTC versus State oversight of sports contracts. While Dan focused on some of the surface level shortcomings of the CFTC relating to consumer protection, Jason made a larger point about how a federal construct would lead to lower prices for customers. Ultimately, Jason aptly categorized the distinction as 'Capital C' Consumer Protection (regulatory requirements and safeguards) versus 'Lowercase c' consumer protection (competitive market forces leading to better pricing and transparency).

“Capital C” Consumer Protection (regulatory requirements and safeguards)

States require their operator licensees to undergo extremely strict certifications regarding responsible gaming controls. Operators must give users the ability to limit usage based on time, spend, or deposits, as well as the ability to “cool off” for a customized amount of time. These requirements come from a good place. However, operators must use extremely specific responsible gaming messaging which introduces an immense amount of complexity in national advertising. Finally, operators must be clear as to what prices are being offered to the user, operators can’t accept trades in an event that has already resolved, to name a few.

All of what’s described above seems simple enough, however, there are not clear requirements around this topic for DCMs. Various DCMs offer consumer protection primarily through optional programs put together, some which have stronger stances than others. This is an area where a risk-based approach may need some more clearly defined guidance. The void of more defined guidance coupled with operators moving quickly into the space has created some obvious areas for improvement.

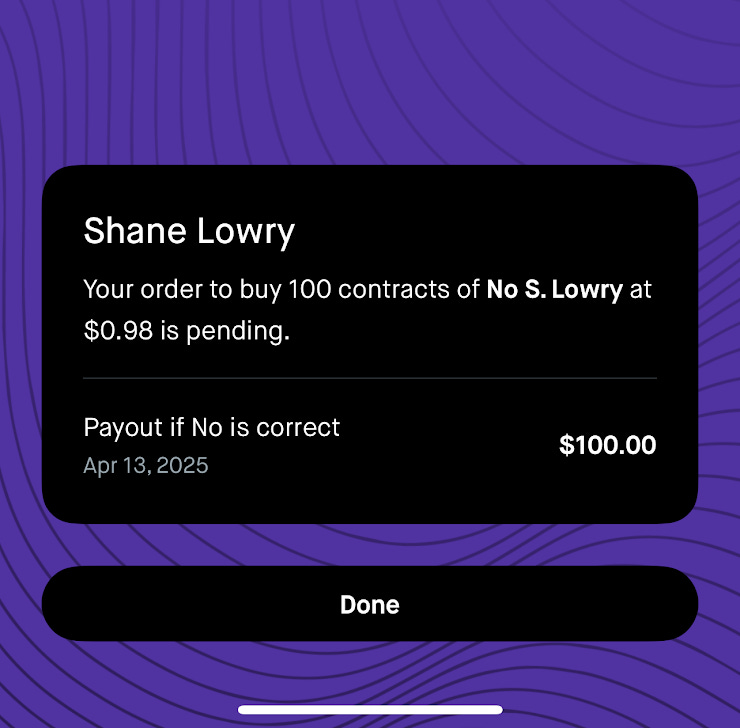

Here’s one: A 100 contract trade placed on Robinhood on Shane Lowry NOT to win the US Open at a price of $0.98 per contract, after $0.02 fees per contract, means the user is risking $100 to return $0 if Lowry wins, and return $100 if Lowry does not win. In no circumstance does the user stand to win money.

Additionally, on the day the Pope was announced, Kalshi may have accepted trades after the information of who was selected became public, as reported by Jeff Edelstein in InGame.

The nod here goes to the States. Users absolutely should be afforded the ability to limit their use of a product, and operators need to have basic rules in place to prevent users from placing trades that can’t possibly win.

Fortunately, some basic rules requiring customer-facing licensees to provide basic protections against unfair practices, and tooling for users to control their use would be easy for the CFTC to implement, and would have broader benefits to futures trading more generally. Something like:

Customer-facing platforms shall not route or accept trades on an event contract after the result of the underlying outcome has been unequivocally determined.

Customer-facing platforms shall not route or accept trades on an event contract at a price that, after applicable transaction fees and commissions, doesn’t give all parties to the trade a chance to profit from the result of the underlying event.

Customer-facing platforms must give users the ability to control their play by setting position, time, and deposit limits for event contacts.

Customer-facing platforms offering more than just event contract trading must give users the ability to opt-out of event contract trading entirely.

“Lowercase C” consumer protection (competitive market forces leading to better pricing and transparency)

Market purists ascribe to the belief that the ultimate form of consumer protection is competition. When it comes to sports betting, we feel this is largely true.

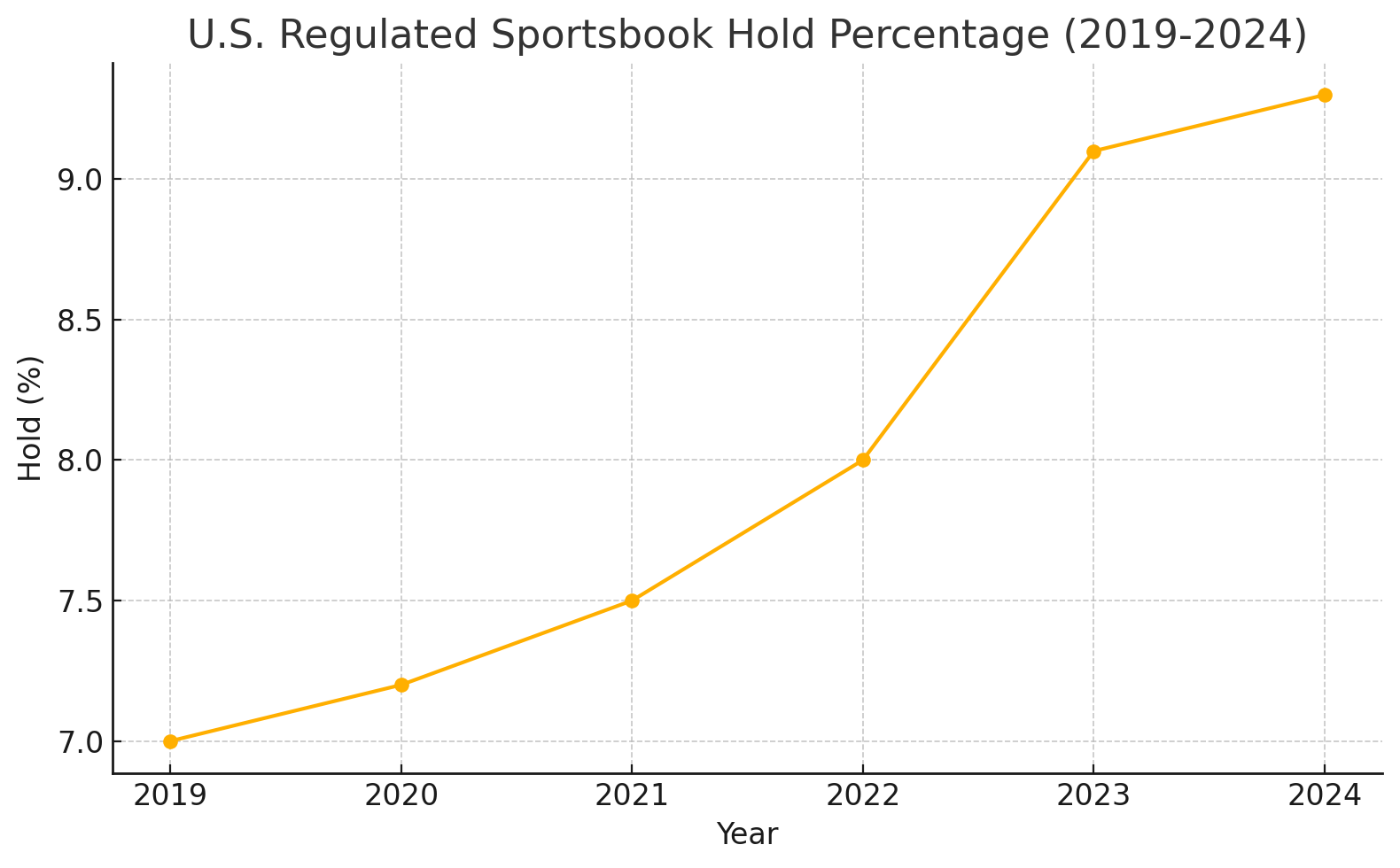

While significant attention is paid towards responsible gaming policies, regulation, implementation, and partnerships, almost no attention is given towards the percentage of each dollar consumers bet is lost to the sportsbooks. Known as the “hold rate”, this percentage tells us the cost of each sports bet. A hold rate of 5% means for every $100 bet by patrons, $5 is kept by the sportsbook. To us, the hold rate is a key determinant of lower-case “c” consumer protection.

Since the introduction of legal sports betting in the US, the hold rate has more than doubled, from 5% to over 10% in 2025. And that’s not all, market leaders like Fanduel note they’d like to increase that cost another 60% to a 16% fee per dollar bet by 2030. As a regulated market matures, you would expect cost efficiencies to increase, not decrease. And yet we’ve heard nary a footnote mention from states on this topic. In fact, states like Tennessee have in the past fined operators for not charging enough per bet (in their case, a 10% fee).

Perhaps no attention is paid to the rising cost because the casino and sportsbook-based version of sports betting isn’t set up for competition or competitive forces. After all, states tax operators based on how much money customers lose. In states like New Hampshire legislators have opted for monopolies with the aim to maximize tax receipts. Just recently, Rhode Island failed to advance a bill that would have opened up their market from a monopoly to a competitive one.

Whereas states primarily view sports betting as a tax driver, and thus pay little attention towards setting up a market to maximize competition and reduce costs for patrons, nearly the opposite could be said of the CFTC. Historically, the futures industry has benefitted from immense competition from all participants as encouraged by the Agency via its core principles.

If you’ve read this far: 1) congratulations, and 2) you’d know that the CFTC is far better equipped encourage a market structure that is truly competitive, and thus present patrons far more consumer protection.

How competitive? We estimate that the long-term hold rate in a federally regulated sports betting market would be sub 1%, even inclusive of parlays.

Economics: Taxes, Fees & Cost to the Consumer

This is where the differences become incredibly stark and directly impact a venue's viability and, ultimately, the prices offered to consumers.

Federal Excise Tax:

DCMs: 0%.

OSBs: 0.25% of all "handle" (total amount wagered) is paid to the federal government under the IRS. This tax on turnover, irrespective of profit, is a significant drag on trading.

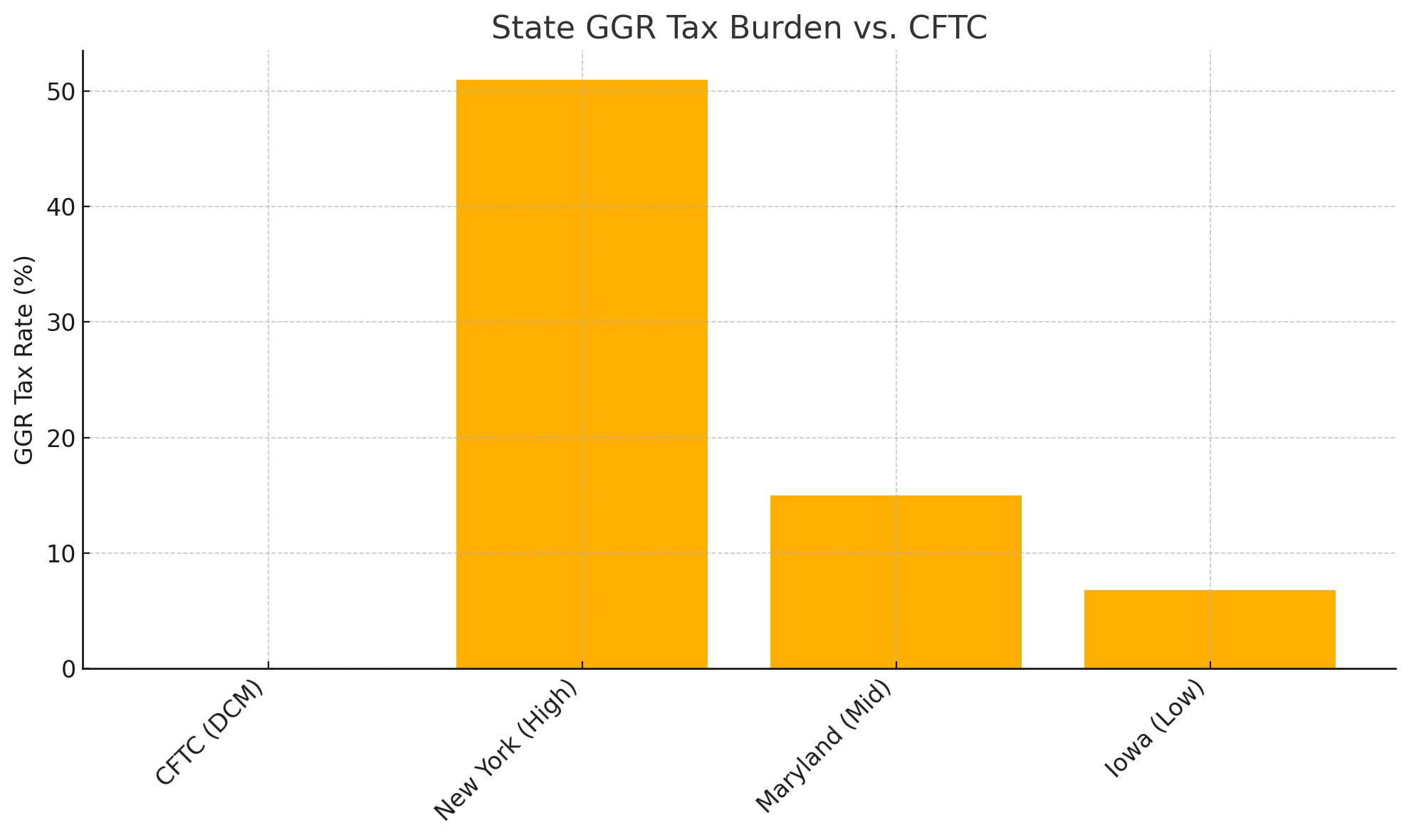

State Gross Gaming Revenue (GGR) Taxes:

DCMs: 0%

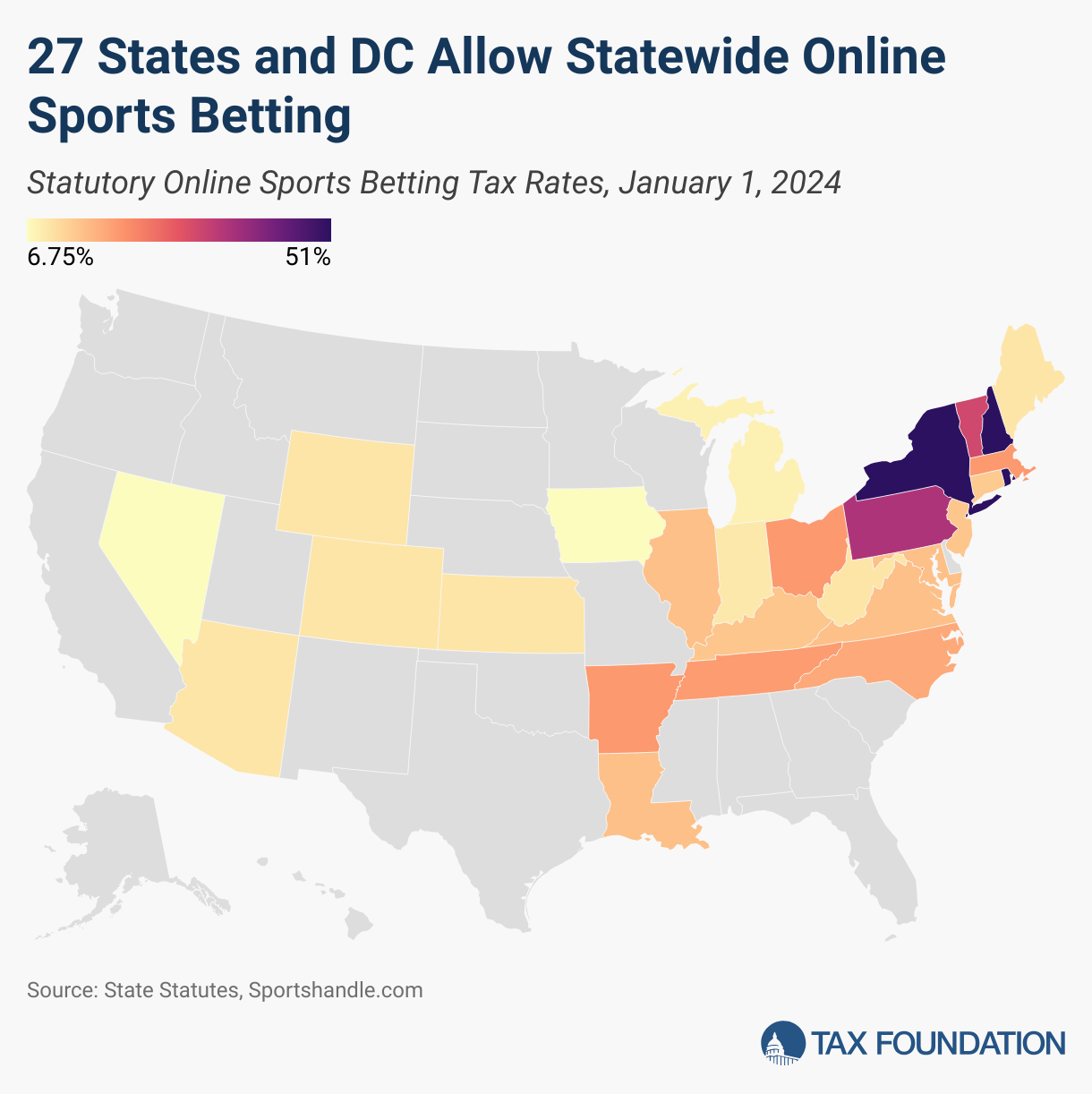

OSBs: Face state GGR taxes ranging from 6.75% (e.g., Iowa) to a staggering 51% (New York, Rhode Island, New Hampshire). This is a direct tax on the sportsbook's revenue before most operational costs and promotions.

Loss Carry-Forward:

Some states (e.g., North Carolina, Illinois) require operators to remit GGR tax even in months where they are carrying a net loss from a prior month (e.g., if bettors have a particularly successful month). This "heads I win, tails you remit anyway" approach adds financial pressure.

Payment Processing Costs:

DCMs: Because their transactions may not be coded as "gambling", they generally experience lower credit/debit card processing fees and fewer declined deposits from issuing banks. Also, as you process significantly more volume across 50 states, processing costs go down per transaction.

OSBs: Can fall under "high-risk" merchant categories, leading to interchange fees that can be up to several times higher than standard transactions.

Certification & Compliance Overhead:

As mentioned, the "one federal submission vs. 50 state builds" dynamic for any platform updates creates massive ongoing cost discrepancies.

Net Effect on Consumers

The combination of lower taxes, reduced payment processing fees, and streamlined national distribution gives DCMs a profound economic advantage. This structural efficiency should translate into:

Tighter bid/ask spreads due to lower fees charged

More capital available for innovation and improved technology. For OSBs, high tax burdens and operational costs inevitably pressure them to maintain higher hold percentages (the inherent profit margin built into odds) to remain viable, which means comparatively worse pricing for bettors.

Initial & Ongoing Technical Certification

Prior to launch, states require operators to undergo a technical certification with their own certification lab, or a contracted third party. The certification can take between two and eight weeks, and is used to ensure that the operator is in compliance with all rules and regulations, including for the mobile apps/website, backend, and all revenue/financial reporting. The certification also tests the geolocation tracking ability of the platform against the state’s borders.

During the testing and certification process, the operator must remain in a code freeze, as any updated codes in new releases will be subjected to regression testing before the initial approval is granted. Depending on the size of new releases, operators can be required to notify regulators of code changes before they are released to smaller releases just requiring a release note.

The CFTC on the other hand requires DCM applicants to demonstrate compliance and commitment to its Core Principals during the application process. Additionally, applicants must walk through all aspects of the user experience with the Commission before they are permitted to go live.

The nod here goes to the CFTC. Once again, the challenge of trying to comply with 38 different sets of rules with regards to initial and ongoing technical certifications only serves to limit the amount of operators with no real benefit for consumers. Additionally, making significant enhancements to an existing software system is much easier with the CFTC than it would be in receiving approval in each gaming jurisdiction.

A Market Still in Motion

The regulatory divide between federally regulated DCMs and state-licensed sportsbooks is far more than a legal or jurisdictional technicality, it’s a foundational difference in how we choose to govern the future of sports trading. While the CFTC model offers national reach, operational efficiency, and a market-based ethos rooted in competition and innovation, the state’s well-intentioned and rooted regulation has struggled to evolve. It remains fragmented, rigid in its structure, and increasingly out of step with the pace of innovation and the demands of modern market-based trading.

Despite all we’ve unpacked, this story is far from over. For investors, operators, and participants alike, the only safe bet is that the rules of the game will keep shifting.